The Land of the Rising Sun

Written by Paul Siluch

February 22nd, 2023

To North Americans, Japan and China are close neighbours with many historical ties. For example, Japan’s writing system uses a form of Chinese symbols, and both countries share similar architectures, food, literature, religion, and laws.

However, they have also been at war with one another many times over the centuries. Both are very strong-willed cultures.

Japan lives in China’s shadow today, yet it was Japan that recovered first after WWII. The U.S. invested the equivalent of $18 billion between 1946 and 1952 to rebuild and modernize Japan such that, by the 1960s, the country of the Rising Sun flooded the west with low-cost goods. Just as China is doing today.

In the 1970s, Japan moved from cheap toys to cheap cars as Toyota, Datsun (now Nissan), Honda, and Mazda took market share from the American giants. They moved to electronics and did the same thing in the 1980s.

Japan rose as America’s economic rival during the 1980s, which made the nation the bad guy in many books and movies of the day. Michael Crichton (“Rising Sun”), Tom Clancy, and Clive Cussler all cast Japanese businessmen as evildoers intent on taking over the world. In 1989, half of the 20 biggest companies in the world (by market value) were Japanese. Private schools switched to Japanese as a second language.

Japan’s stock market crash of 1989 ended all that. Japan’s Nikkei 225 fell 65 per cent in just three years and continued lower until it was down 80 per cent by 2003. Its banks had grown to be global titans based on the inflated values of its real estate, and “Keiretsu” companies – cartels that shared cross-ownership with one another in incestuous webs – filled the rest of their balance sheets.

As everything – stocks, real estate, loans – deflated in price, bank balance sheets became saddled with assets worth less than they paid for them. The banks hid these bad debts with fictitious markups and carried them forward year after year, hoping for recovery. With too much debt, Japanese banks made fewer and fewer new loans, choking off the country’s growth.

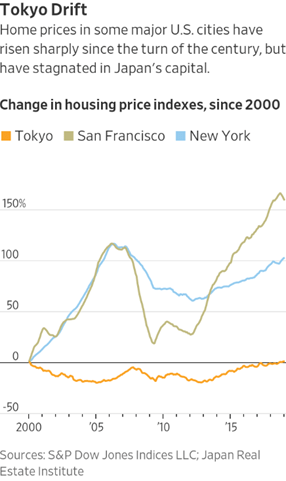

This lack of growth is reflected in real estate prices. The Wall Street Journal published this graph in 2019 showing how real estate prices had risen 100-150 per cent in the US over 20 years (and even higher since 2020) while Tokyo homes barely budged. Now, blame their shorter-lived wood frame construction and aging population creating more vacancies, but Tokyo’s population actually went up during those years.

Canadian and U.S. banks have been eager to lend money for mortgages on homes, even after the 2008 real estate collapse. Not so for Japanese banks. They took on so many bad loans in the 1980s, and carried them for far too many years, that they became very tight-fisted in their lending. Housing is seen as a poor place to invest because you are selling today at the same price as 20 years ago.

When we think of growth today, we think of Asia without Japan. There is even an ‘Asia ex-Japan’ index to remove this global laggard! Years of flat real estate prices, bankruptcies (such as Japan Airlines in 2010) and calamities (the Fukushima nuclear disaster in 2011) have taken Japan from a “must-own” in global portfolios to a “why bother?”

There’s an index called the Big Mac Index published by The Economist magazine.

It’s goal? To compare costs across a number of countries in a way that everyone can instantly relate to: how expensive is a Big Mac in your home country?

It is not a perfect test, by any means, but the humble McDonald’s burger does span a number of industries to get to your plate. There are agricultural, labour, and transportation costs. There are the costs of heating and real estate, as well as taxes. A growing amount of technology (ovens, inventory, payment systems) also need to be factored in, so it is accepted – if not wholly embraced – by the economics profession as one way to measure the relative competitiveness of a country.

A Canadian Big Mac on the global index is approximately 15 per cent less expensive than a U.S. Big Mac. The U.S. dollar has appreciated sharply against most world currencies in the last decade, so almost everything down south is expensive for Canadians these days.

But what is interesting is where Japan sits. A Big Mac is over 41 per cent less expensive in Tokyo than it is in New York (source: The Economist):

The Japanese yen is known to be extremely undervalued against most major currencies – the Japanese government has always encouraged exports through a cheap currency. But, Japan also has access to lower-cost Asian agriculture, has far more modest real estate prices to contend with, and has automated many parts of the fast food industry due to its aging population.

A Big Mac is cheap in Japan because the entire country is undervalued.

I came into the investment business when Japanese stocks were roaring and the Imperial Palace in Tokyo was worth more than all the real estate in California. Just as real estate has gone down for decades, so too has the stock market. U.S. stocks have risen ten-fold since 1990 while Japanese stocks are still 26 per cent below that year’s peak:

Now fast-forward 33 years. At its peak in late 1989, Japan’s index traded at 60x earnings. Today? Japan trades for about 13.8x earnings (source: Financial Times). And the value of its assets – the land, buildings, and patents of its companies – are also inexpensive. The leading Japanese stock exchange trades at 1.31x book value versus 4.1x for the US S&P 500 (source: St. Louis Federal Reserve).

Why is Japan such an inexpensive market today? There are a number of reasons:

- The country grew older. The oldest nation on Earth. Just as a new younger competitor – China – entered the world stage. Japan’s population is projected to fall from 127.09 million in 2015 to around 110.92 million by 2040. (In Business magazine)

- Japan is re-arming in the face of rising Chinese aggression.

- Japan became overly reliant on oil imports after the 2011 Fukushima nuclear incident forced the closure of dozens of its reactors.

These are all well-known, however. After years of caution, Japan’s companies are run extremely conservatively. By the end of 2019, Japanese companies had stashed away over US $4.8 trillion in cash (Bloomberg). While most western nations worried about their companies’ borrowing too much, the Japanese government vowed to stamp out cash-hoarding.

On a price/book basis (what the assets of a company trade for), Japan’s companies sit at one of the most inexpensive levels in the world – half of Canada’s stock market and one-third of those in the U.S. (source: Macrotrends).

For value investors, these vices are turning into virtues.

- High cash levels mean dividends are increasing.

- The shrinking population has meant an intense focus on robotics and mechanization.

- Cross-holdings are being unwound, releasing new value as hidden divisions and companies are set free.

- China’s re-opening means exports and tourism are set to improve.

On the energy front, 10 of the 33 nuclear reactors that were closed have restarted with a further 16 in the process of restarting by summer of 2023. Japanese public opinion is now firmly in the pro-nuclear camp due to high oil and LNG prices.

The investing world really sat up in their chairs and took notice when Warren Buffett bought into five of Japan’s oldest trading companies in 2020. He now holds over $11 billion in Itochu, Marubeni, Mitsui, Mitsubishi, and Sumitomo.

Dividend Value

While Warren Buffett sees value in the trading houses of Japan, our interest is in Nintendo, the gaming company. Famous for its Super Mario, Pokémon, Donkey Kong, and Legend of Zelda games, as well as its Wii and Switch consoles, Nintendo’s offerings are family friendly. It has the most widely-used gaming machine in the world (Switch) which competes with Sony (PlayStation) and Microsoft (X-box). Like these other giants, Nintendo has created an on-line store of games and pay-by-the-month service. Recurring revenue is valued much more highly than one-off sales, so we expect valuations to expand.

The shares trade at a modest 12x P/E with a dividend yield of 3.9 per cent, which they can easily afford because Nintendo holds over $11 billion in net cash.

Recurring revenues are rising and a new Switch console is due in the next year or two, which has driven sales higher in the past.

Our portfolios added Nintendo this week.

![]()