Booms and Busts

Written by Paul Siluch

October 10, 2025

The railway boom began with a boom. Literally.

Up until 1768, steam engines were underpowered and risky. They were useful for pumping water out of mines, but due to high pressure and poor-quality iron, early steam engines had a bad tendency to explode.

Along came James Watt in 1769. His efficient – and lower-pressure – steam engines ushered in the industrial revolution (Wikipedia). In particular, the steam locomotive. The railway boom swept across the world with a frenzy of building from 1850 to 1873 in the United States.

Capable of moving goods at less than half the cost of a canal boat, steam-powered locomotives changed the world. They moved people and goods faster than at any time in history. War accelerated the build-out even more, once governments realized how quickly they could move troops, signalling the end of the horse-drawn era.

Railways as an investment scheme moved even faster. Banks, pension plans, and small investors poured their money into rail shares. They were changing the world! No one could lose. In the U.S., 80,000 miles of track were laid by 1873, with 35,000 miles built in just seven years (rail statistics from Library of Congress data).

By 1872, between 50% and 60% of the entire stock market was railway-related shares and bonds. This was a level of concentration that has never been reached since (Visual Capitalist).

In 1873, the biggest financier – Jay Cooke – went bankrupt. He bet big on the westward expansion of America through the new Northern Pacific Railway but passengers were few and freight less than expected. U.S. markets plummeted. Stocks fell 34% over the next two years and 18,000 businesses collapsed (The Panic of 1873, William Ellis).

After the crash, railway planners revealed that 25-30% of all the new track laid was uneconomical. Lines duplicated one another or served markets too small to be viable. Almost one-quarter of all U.S. railroads went bankrupt by 1875 (Wikipedia).

Even little Victoria in Canada participated. We once had three rail lines along the Saanich Peninsula, each less than 20 miles long. All are extinct today - we have bike trails where they once existed.

Despite the glut, most of this “excess” rail was filled within 10-12 years (Origins of the Decline of American Railroads, Albro Martin). And as new cargo filled the empty lines, even more had to be added, this time at a more measured pace. Diesel engines eventually replaced steam engines, so even more cargo could be hauled, and at faster speeds.

It wasn’t really a bust. It was simply too much, too soon.

Now, fast-forward to the late 1990s and the next boom.

The Dotcom Boom

As internet use exploded in the late 1990s, claims of “infinite demand” could be heard echoing up and down the canyons of Wall Street. Everything would be digital and everyone would be connected.

The U.S. alone laid 80 million miles of fibre optic cable to meet this surge, only to find demand growing at just 5-10% per year.

Remember America Online? It was the largest internet provider in 2000 and was still using dialup modems over copper wires. Fewer people were connecting than expected.

Between 85% and 95% of fibre optic cable was empty. It came to be called “dark fibre” because there was no light being transmitted. (All data above: Irrational Exuberance – Robert Shiller)

The dotcom crash resulted in a 40% decline in the S&P 500 from 2000-2002. Many internet companies went bankrupt.

And yet by 2010, most of this “dark” fibre was filled with traffic from new companies like YouTube, Facebook and Google. We had to start laying even more fibre optic cable to keep up.

Again, too much, too soon.

The AI Boom

We are in a new boom. This time, it is artificial intelligence fuelling the frenzy.

How does today compare to the past? Here are the percentages of the stock market concentrated in the “boom” sectors:

|

Era |

Railway (1873) |

Dotcom (1999) |

AI (today) |

||

|

Stock Market Concentration |

50%-60% rail stocks |

33% telecom/tech stocks |

37% AI/semi stocks |

(The Other Half of History, Financialcontent.com)

While we are well below the market concentration of the railway era, the AI boom is already above the dotcom era.

Yes, today’s companies are far more profitable and cash-rich than companies in 2000 were, but they are spending even more heavily. Some estimates show up to $5 trillion is going to be spent on new data centres by 2030, in the race to Artificial General Intelligence (McKinsey & Co.), with little revenue coming in yet to justify this.

- Optimists say there won’t be a bust because AI is making us far more productive.

- Pessimists say we are close to a bust because AI will never deliver the productivity leaps it has promised.

What does the past teach us?

This bubble will pop, but not just yet. There will be exciting inventions in drug discovery, self-driving, and robots, because of AI. There is no sign yet of any bank in trouble.

But there will be a slowdown in this relentless pace of spending because nothing can grow like this forever. AI spending has propped up the U.S. economy and when it falters, so too will stocks and employment.

At some point we will go too far, too soon, like all past booms have. We will be swimming in data centres, chatbots, and AI models. They will seem like a giant waste of money.

And then?

Within a decade, new companies will arise to utilize the excess. We don’t know who they will be or what these companies will do, but they will appear. They always do.

Where the Bargains Are

While we still hold several of the technology giants involved deeply with AI, we are also keenly aware of the vacuum they have left behind. By sucking most of the ‘investment oxygen’ out of the room, many other sectors have become underweight in portfolios.

Defensive companies, such as consumer staples, beverages, alcohol, and cleaning products, have all but been ignored.

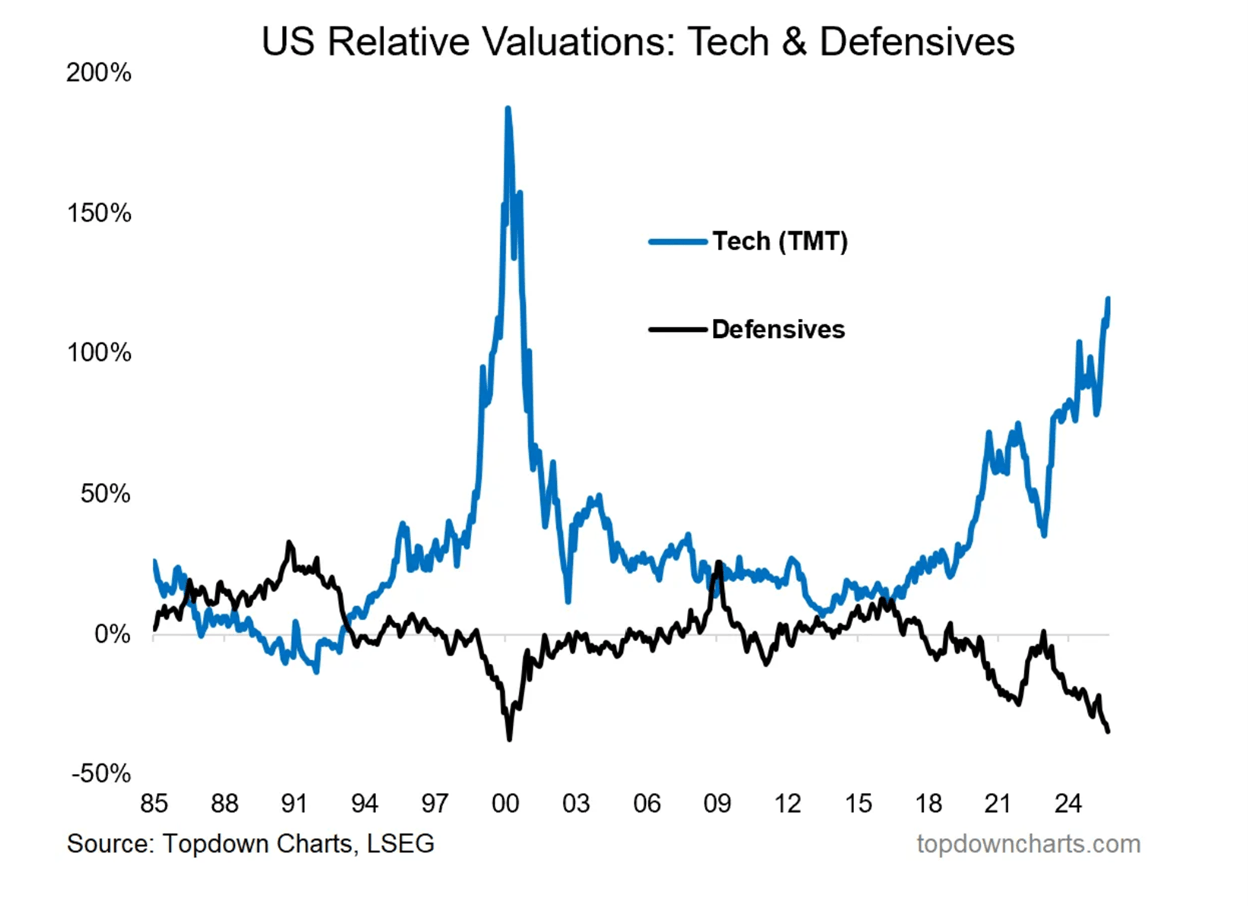

This chart above shows the relative valuation spread between these groups. More importantly, it shows the deep undervaluation of many defensive companies.

For example, U.S. drug stocks. Once investment darlings, they have been sliced in half (or more) based on price-gouging accusations and a decline in new blockbuster drugs.

Just last week, we watched the entire sector jump, as the White House announced a deal on drug pricing. It was less harsh than expected, and many of the giants like Merck and Pfizer rose 9% in a single day.

Water utilities and food companies are showing up on our radar as well, reflecting the same undervaluation the chart above depicts. Who needs water and food when you have ChatGPT?

In every bust, the seeds are sown for the next boom. We saw this in 2000 when telecom stocks faltered and defensives began a long rise.

If the AI-centred technology companies ever do decline in price, we may see the same thing play out all over again.

![]()