Another War

Written by Paul Siluch

March 19th, 2026

In case you missed it, there’s a Middle East war going on. Another one.

Depending on your political viewpoint, this war is either completely unjustified due to violations of international law or completely justified because a nuclear threat is being removed. As investment advisors, we remain neutral. You can’t be a hawk or a dove in this business. Politics and emotion don’t mix well with money.

The 2026 conflict centres in Iran, although markets are nervous because multiple countries are now involved.

What is it that Iran has that the world would miss due to war? Iran is one of the world’s largest date producers, so expect the price of dates to rise in the months ahead.

But markets don’t fall because of a date shortage. Iran also produces about 4% of the world’s oil (Goldman Sachs) and controls the Strait of Hormuz in the Persian Gulf, where 20% of global oil passes.

The world still runs on oil, so this is what is spooking markets. The loss of 20% of the world’s oil could send oil prices above $125 per barrel, triggering recession in many countries.

Some of you will remember the oil spike in 1973. Prices rose from $2.90 to $11.65 – a fourfold increase. The Gulf War in 1990 saw a doubling from $17 to $36, which also caused markets to fall (IEA).

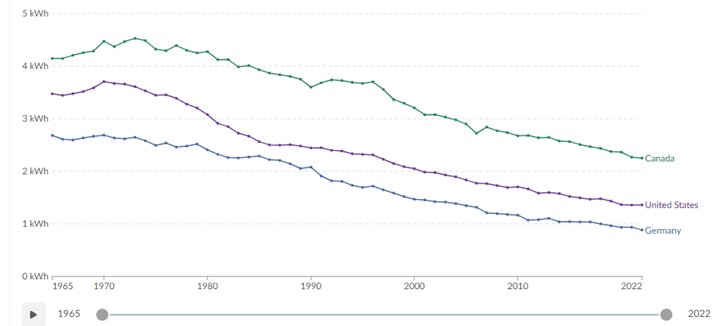

The world today uses less oil to grow. The amount of energy consumed per unit of growth in the economy (GDP) has fallen by half since 1970. Our cars (many electric now), refrigerators and home heating are far more efficient. Rising oil prices hurt us less.

Energy Intensity – Energy Consumption per unit of GDP Our World in data: US Energy Information Administration

Our World in data: US Energy Information Administration

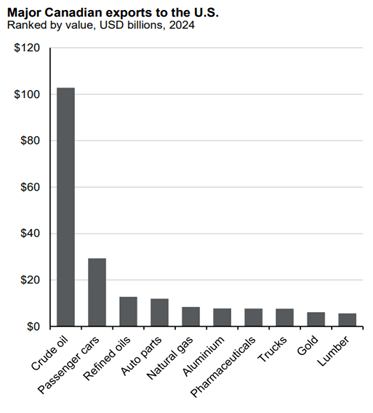

Canada is a large energy exporter. Despite our efforts to diversify, our largest exports are oil and natural gas to the U.S. – 25% of Canada’s exports are hydrocarbons (worldstopexports.com). We should be immune, right?

JPMorgan Asset Management

JPMorgan Asset Management

Canada is less exposed, but not immune to economic shock. Why?

Rising oil prices push inflation higher, which pushes interest rates higher. Both Canadian housing and overall borrowing are stuck because of high interest rates. Higher borrowing costs are the last thing we need because it could lead to a mild recession.

So, the stock market is falling to adjust to the possibility of higher inflation and slower growth.

That’s the bad news.

Wars tend to cause market jitters for a short period of time. Going back to 1941, here are returns due to 24 wars, bombings, assassinations, and invasions:

- Worst: -20% decline, 10 months to recover losses (1941)

- Average: -5% decline, under 2 months to recover losses

Bloomberg, Manulife

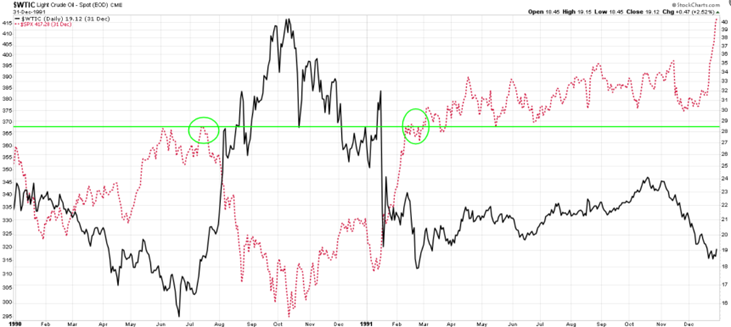

The biggest decline I remember was when Iraq invaded Kuwait in 1990. Oil prices rose from $16 to over $40. The market fell by 20%. Markets (red) rallied back within six months as the threat of oil (black) shortages vanished and energy prices came down.

Oil production can increase in other parts of the world. This takes time, but high prices are always met by higher supplies. This time will be no different.

Finally, the second year of the presidential term is often the worst of the four-year term. And 2026 is right on cue.

Holding tight and collecting dividends is the best course of action, if history is any guide. Wars and threats to oil supplies are sudden, painful, and almost always temporary.

This, too, shall pass.

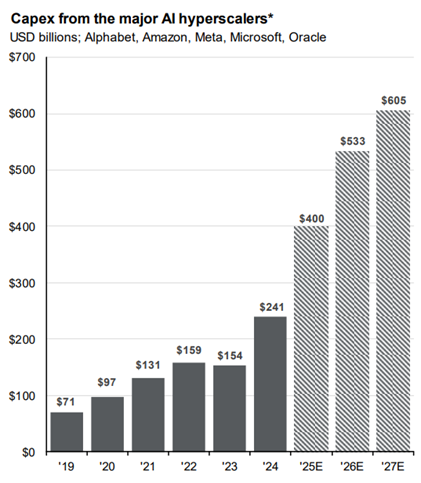

Meanwhile, we must remember the most significant trend that will not be interrupted. With the rise of artificial intelligence, we are building data centres at an accelerating pace. We need chips, copper, workers, and oil to do this.

Bloomberg, JPMorgan

Bloomberg, JPMorgan

Paul Siluch, Sharon Mitchell, Peter Mazzoni, Lincoln Jiang - Raymond James (Canada) Ltd.

![]()